When it comes to fundraising, there are several options for startups. SAFEs have become popular in the last years to quickly add cash. While they might be tempting at an early stage, they can turn into a nightmare for founders and investors later on.

When you buy or sell something, you want to agree on a price, don’t you? It is probably the most essential variable for your final purchase or sales decision. It would just be crazy, for a buyer of a house, for example, to say: ‘Hey, why don’t I give you some money now so I know that I own a piece of your house and we see what exact price I pay for this piece and how big it is later on when somebody else invests?’ Weirdly enough, this is exactly what SAFEs (and to a lesser extent convertible loans) are like – and we are seeing more and more of them recently…

While SAFE (Simple Agreement for Future Equity) notes are interesting at the earliest stages of a company or for smaller bridge rounds, they can quickly fuck up the cap table of a young company and turn into an absolute nightmare for founders and (potential) investors. I’m not a big supporter of SAFEs and convertible notes. Recently, I had to cope with several founders of exciting young companies who struggled with them. The SAFE rounds these founders had already raised created a massive headache to make a proper equity round happen at a later point in time. Here’s why theses financing instruments are usually not a great idea.

What are SAFEs and Convertible Loans, and what’s the difference?

SAFE notes have become popular in the past ten years. They are a simple way for startups to raise capital without encumbering their balance sheets with debt – unlike convertible loans. Their terms are generally also less onerous than you would find in convertible debt instruments. SAFEs do not give companies a free ride though. Where there is no debt, there can be no security and, generally, no repayment on a defined maturity date. In case of a SAFE round, there will usually just be a discount on a future funding round, and sometimes, but not always, a cap on a next equity conversion valuation. What SAFE notes and convertible loans both have in common though is the underlying intention that the amounts invested will be converted as part of the next qualifying financing round. On top of that, convertible loans usually demand the repayment of the loan or automatic conversion at a defined price (these usually have a cap and sometimes a floor) at a specific maturity date (if there is no qualified financing round).

Are SAFEs a good or lousy instrument to raise capital?

Our team at Mangrove Capital Partners has done investment rounds in startups with SAFEs in the past. As venture capital investors, we are not strictly opposed to them. But founders need to know what they are up against. In general, SAFEs are really bad for raising relevant financing rounds, especially if they exceed an investment amount of EUR 1M-2M. Why? Because just like with the example of buying a house, there is no final price. As a result, they defer the most critical investment terms (valuation and founder dilution) to a later stage – this is a huge problem. Founders should know precisely how much of their company they own at every moment of their startup journey. ‘Price’ is always a tricky topic, and SAFEs just avoid it by merely kicking the can down the road.

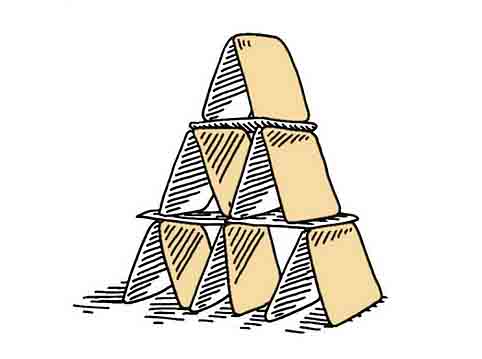

Good investors will also have an idea of how to price your business and can articulate their rationale when making a deal. Smaller rounds by angels, friends, or family are different though. These are often done via convertible debt. It makes sense that such investors at the earliest stage would not want to enter into a tough negotiation with a founder and prefer to only pick it up when professional investors enter the equation. Avoiding the price discussion in the beginning makes things so easy at first that founders can get sort of ‘addicted’ to SAFEs and raise a couple of them on top of each other… sometimes even with different terms! This goes on until (inevitably!) a price for a funding round actually happens. SAFEs then start crashing into each other like a house of cards, making a clean round nearly impossible.

What are potential downsides of SAFEs for founders?

To be clear: The biggest losers out of all of this are usually the founders. Without an agreement on price, SAFEs can put founders in the tricky position of promising investors a potential amount of ownership. Some months later though, they sometimes cannot deliver on this promise when the notes convert. By the same token, founders think the SAFE cap should be the minimum valuation of a next round and will be disappointed when they realize it was unrealistic. Many founders who raised SAFEs last year now have to see their valuation drop much lower than expected… If the size of SAFEs is too big, you have a serious founder dilution issue.

Our team at Mangrove highly recommends founders to do priced equity rounds. It does not take much longer and the legal costs are acceptable as well nowadays, especially early on. If you or your investors want to invest via SAFEs nevertheless, make sure you do not raise more than EUR 1M-2M until the next financing round. Be transparent with your investors and yourself on future cap table scenarios after a conversion as part of a next funding round.

After all, with markets calming down, I guess we will see fewer SAFEs in the next 24 months, particularly those with no warrants and/or valuation caps…

→ Want to know when it actually makes sense to use SAFEs or Convertible Loans after all? Head over to Yannick Oswald‘s blog ‘Opportunities Everywhere’ to read the article in full length.