The new Corporate Sustainability Reporting Directive (CSRD) marks a significant milestone in sustainability reporting, promising to establish a new era of transparency and accountability for EU companies.

With the focus on utilizing the developing European Sustainability Reporting Standards (ESRS), this directive seeks to form a structured and harmonized framework for ESG reporting across Europe, and with that reduce the reporting costs for companies. With the new regulations, investors and other stakeholders can demonstrate their commitment to sustainability in a more impactful manner, as they are now equipped with the necessary information to evaluate investment risks that may arise from climate change and other sustainability concerns.

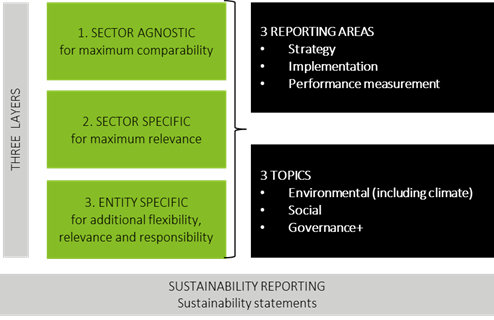

The ESRS aims to boost transparency by requiring detailed ESG data and standardizing disclosures regarding strategy, implementation, risks and opportunities, as well as performance measurement of ESG KPIs. Information disclosed under the ESRS must be relevant, comparable, verifiable, understandable, complete and accurate, so that stakeholders have a good overview of the sustainability-related information disclosed.

The ESRS focuses on three reporting layers of sustainability information:

- Sector agnostic: providing a common base for all reporting entities ensuring comparability;

- Sector specific: promoting relevance and peer comparison per sector;

- Entity specific: taking each organization’s particularities into account.

Currently only the draft for the sector agnostic ESRS has become publicly available and was submitted to the European Commission. The draft placed emphasis on the environment, social and governance topics, while it also established mandatory standards for preparing sustainability reporting under CSRD. These standards intend to enhance stakeholder understanding of ESG information disclosed and the impact that companies have on ESG themes, the material risks and opportunities regarding these issues and their impact on the generation of enterprise value.

How can companies effectively disclose their ESG data?

To comply with CSRD regulations, companies must conduct a materiality assessment to identify the appropriate disclosure standards. This means that this double materiality approach requires companies to both examine how their operations impact people and the environment and also how people and the environment can affect their operations. This is a unique feature of CSRD, which will encompass all ESRS-focused disclosures.

After conducting the materiality assessment, companies will have to delve into the relevant ESRS and identify the disclosure requirements and datapoints to report on and to develop specific processes and strategies to efficiently collect relevant data and information in order to implement these requirements and avoid potential risks.

Limited availability, consistency and reliability of the data required for some disclosures will be a pivotal challenge in sustainability disclosures aligned with ESRS. This is particularly important due to the mandatory issuance of limited assurance by third-party providers which will be required as of the ESRE implementation date. Small and medium enterprises will especially struggle because they lack the relevant structures to meet ESRS reporting requirements. Therefore, companies should start formulating the relevant processes to collect this sustainability data and implement more reliable data collection tools.

Under these new standards, companies will be required to elevate their sustainability disclosures. They will need to expand their horizons when it comes to reporting sustainability efforts and finding new ways to collect ESG data. Continuous improvement will be key, as companies must stay abreast of the evolving sustainability scene.

Special thanks to Melina Gkiolma for her valuable contribution to this article.