It’s that time of year when we start to see annual round-ups and evaluations from different industry groups. When it comes to the tech space in Europe, one of the definitive reports is Atomico’s ‘State of European Tech 2021’. We’ve put together a summary of the most interesting observations from the last year. One thing’s for sure, Luxembourg is starting to see its contribution to the growth of tech in Europe recognised.

Luxembourg’s contribution recognised in several areas

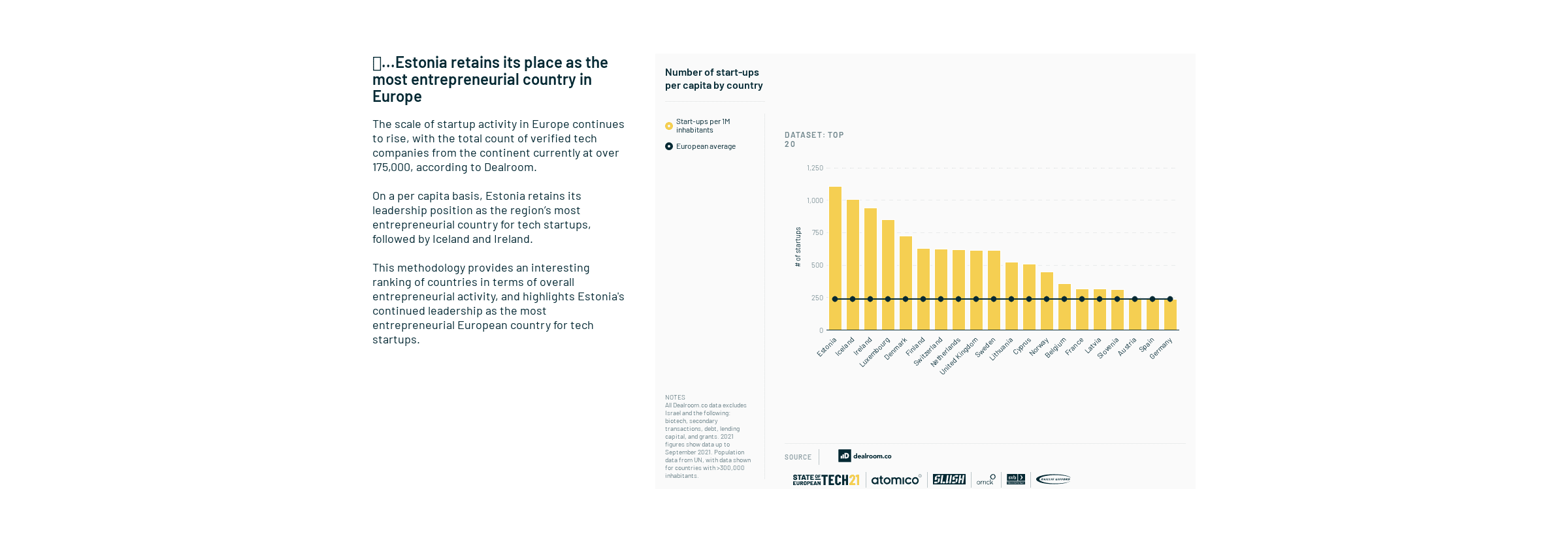

Whilst the top five tech hubs of London, Berlin, Stockholm, Munich and Paris still dominate, we are seeing once-small players provide some competition, and new players emerge. We’re also seeing Luxembourg rank quite highly in a number of areas. When it comes to the number of startups per capita by country, Luxembourg is right up there at number four.

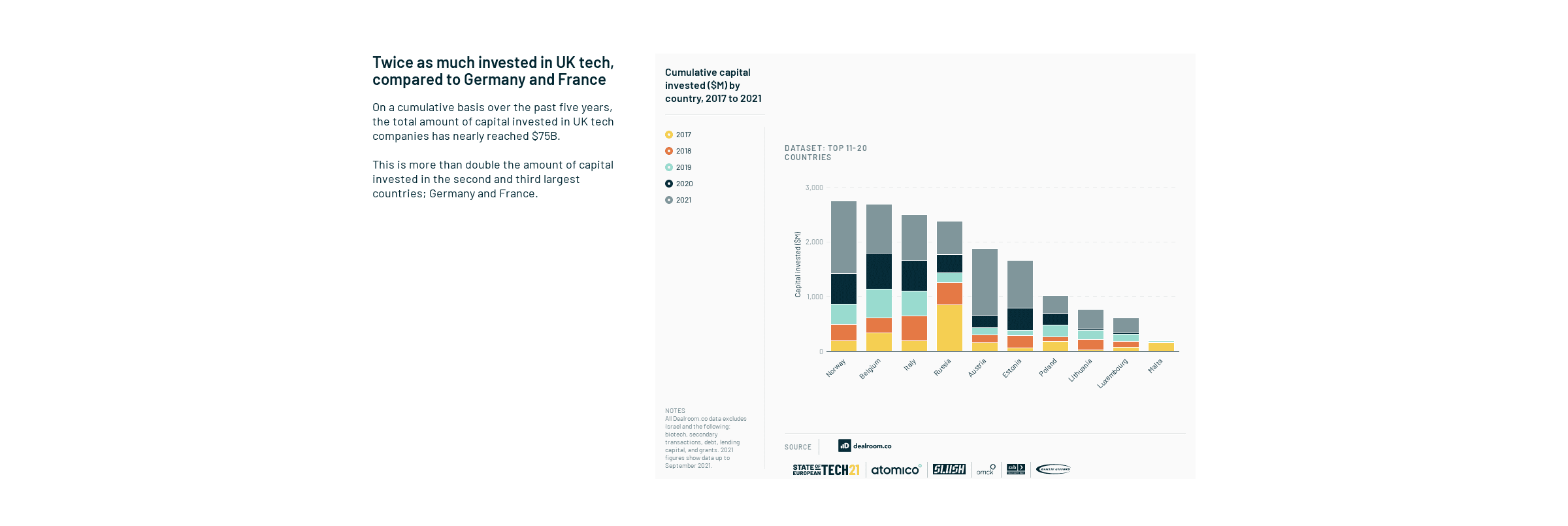

It also appears in the top 20 when it comes to European country hubs by capital investment (based on 2021), and when it comes to cumulative capital invested, between 2017 and 2021. The amount for this in 2021, stood at $268m.

This could have been driven by the growing interest in fintech. In 2021, this sector had the most significant increase in investment and, along with health and B2B software, were key thematic focus areas of new funds raised.

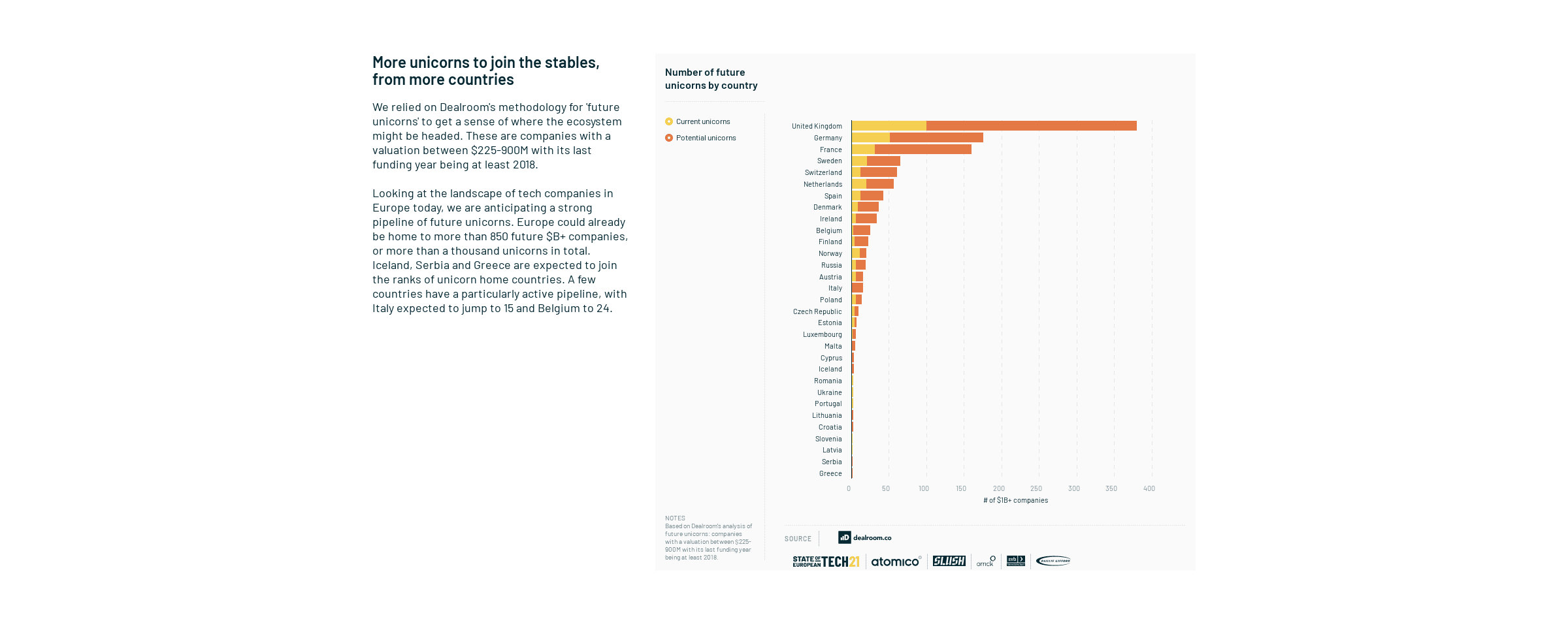

Another area where Luxembourg has seen improvement is when it comes to the number of predicted unicorns. Whilst the country ranks quite low when it comes to the number of $1b+ companies – currently 21st with 2 VC backed unicorns – the future looks brighter. Based on the current startup landscape in Luxembourg, there could be three potential unicorns in the pipeline, placing the country 19th in Europe.

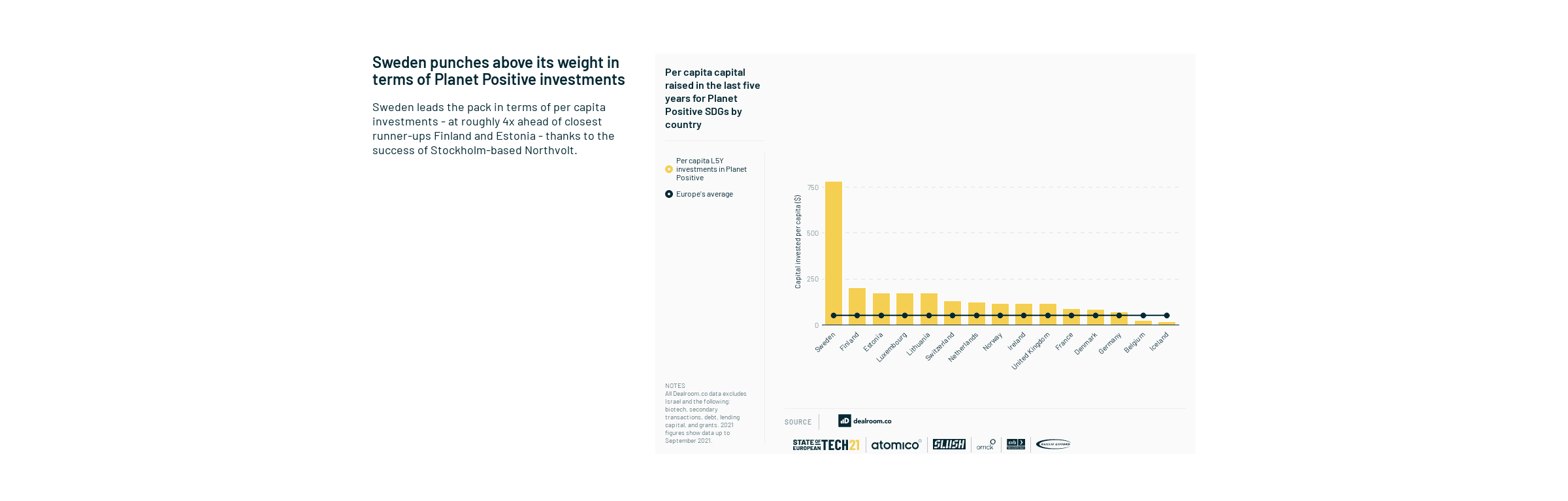

Finally, Luxembourg scores highly when it comes to sustainable investment. In 2021, the country ranked 4th in Europe when it came to per capita capital raised in the last five years for Planet Positive investments.

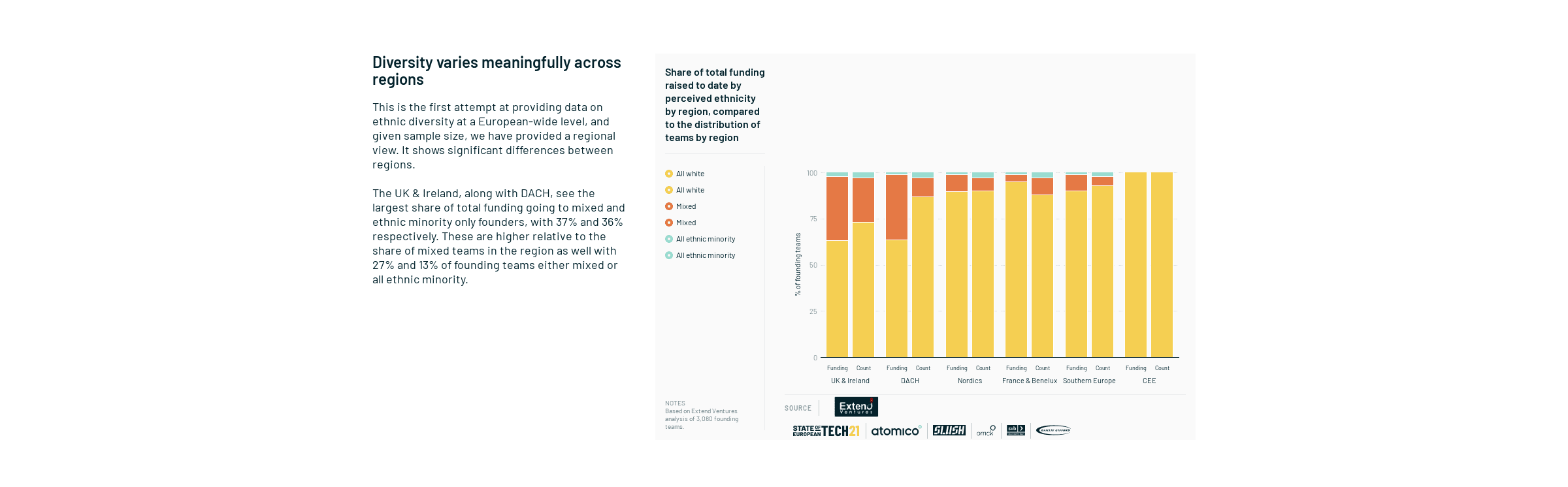

However, despite seeing steps in the right direction when it comes to sustainable development, the wider Benelux and France region are lagging behind other regions when it comes to diversity. The majority of the funding still goes to all-white teams, which is disproportionate to the number of teams with mixed or all ethnic-minority teams.

But what’s the state of European tech more broadly?

Europe hits its stride in 2021

According to Atomico, in 2021, Europe firmly positioned itself as a global tech player. $100bn of capital was invested and European tech created value at its fastest pace, adding $1tn in 8 months. 98 new unicorns were created, and not only is that number increasing, but they are scaling faster too. The first European company founded in 2000 took 6 years to scale to unicorn status, however for companies founded in 2018, it only took one year for the first two companies to reach $1bn.

To top it off, Europe’s startup pipeline is now on par with the US, suggesting the future looks even brighter. According to Stripe Co-founder & President, John Collinson, “5 years ago, you could fit all of the continent’s unicorns in a dining room and decry Europe’s missing tech giants. Today, you’d need an auditorium with 321 seats…”

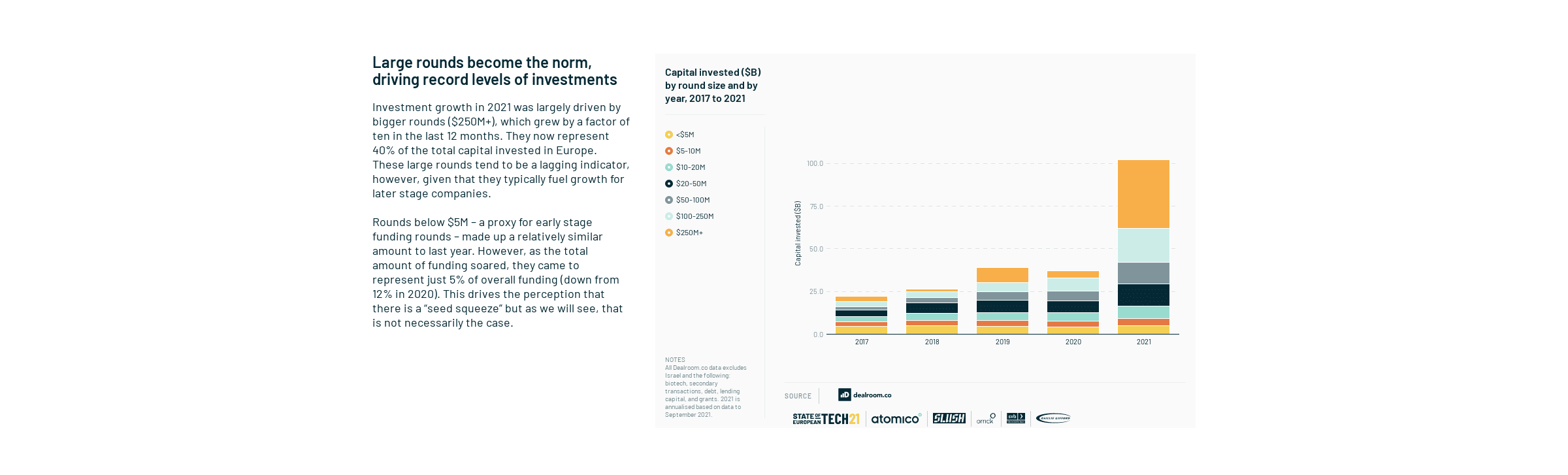

Large funding rounds have become the norm in Europe, and have record levels of investment. 40% of the total capital invested in Europe came from rounds of $250m+. In 2021, more than 5x the number of rounds were for more than $250m, than in 2020.

2021 was also a groundbreaking year for exits too. The record exit value is more than $275bn. 51% of this ($140bn) can be attributed to VC-backed companies, across IPO’s, direct listings (60% combined), M&As and SPACs.

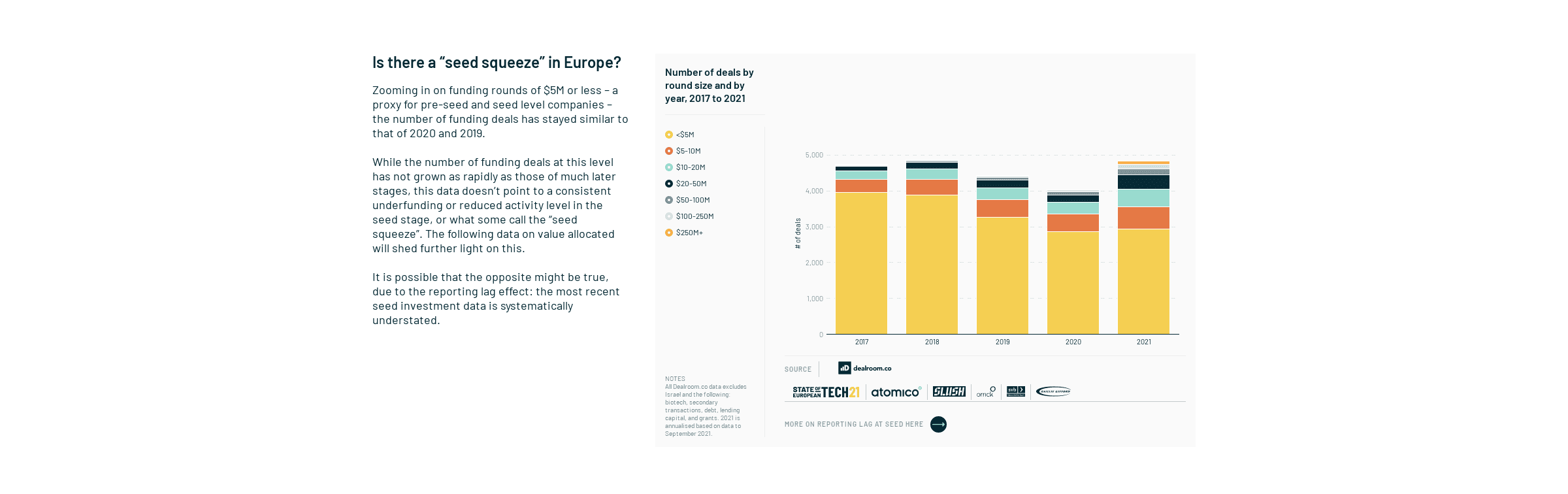

Whilst the “growth stage” funding gap is closing – it has increased by around 5x in the last 5 years – early stage funding only increased 2.3x in the same period. Pre-seed and seed funding is also seeing stagnation, with the number of deals at this early stage staying similar to 2019 and 2020 levels.

The European talent pool is deeper and more experienced

When it comes to people, particularly founders, Europe is once again seeing success. It has the strongest ever talent pipeline, with early-stage funding on par with the US. Whilst there is a big pool of veteran talent to choose from – 38% of founders and leaders have previous experience at more than two tech companies – investment is also being made into the new generation of tech leaders.

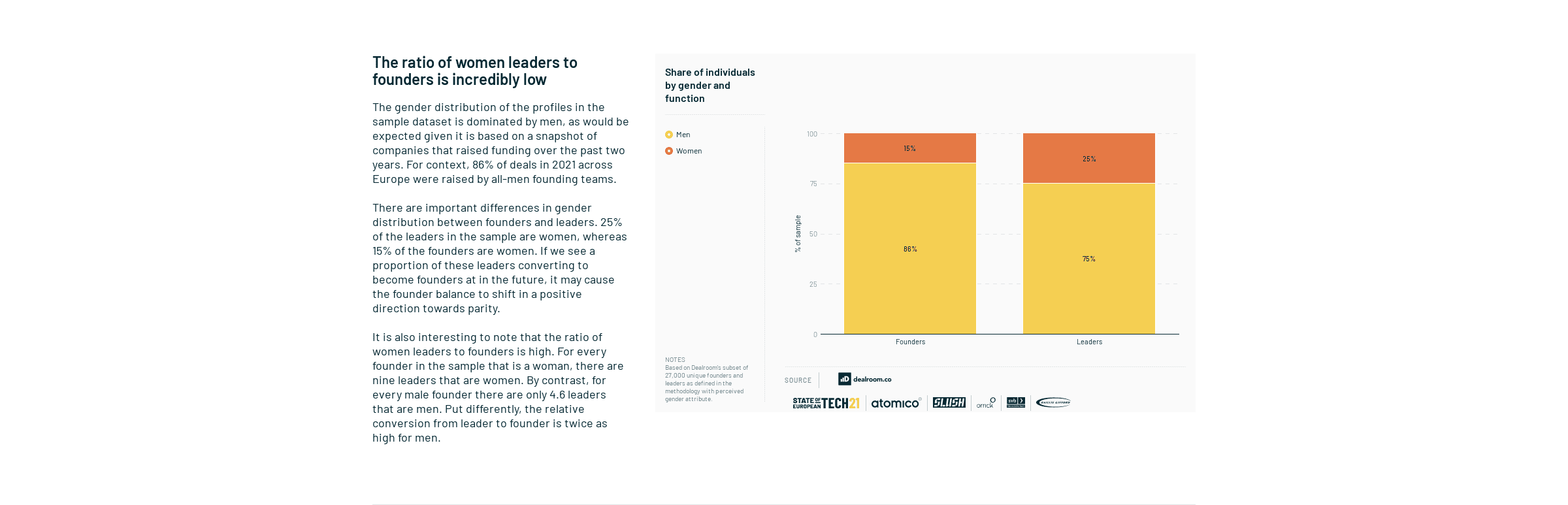

Having said that, there is still work to be done around attracting more diversity within the next generation. The bulk of founders and tech business leaders are men – 86% and 75% respectively, and interestingly, the ratio of women leaders to founders is high. For every female founder, there are 9 female leaders, compared to only 4.6 male leaders for every male founder, suggesting conversion from leader to founder is twice as high for men.

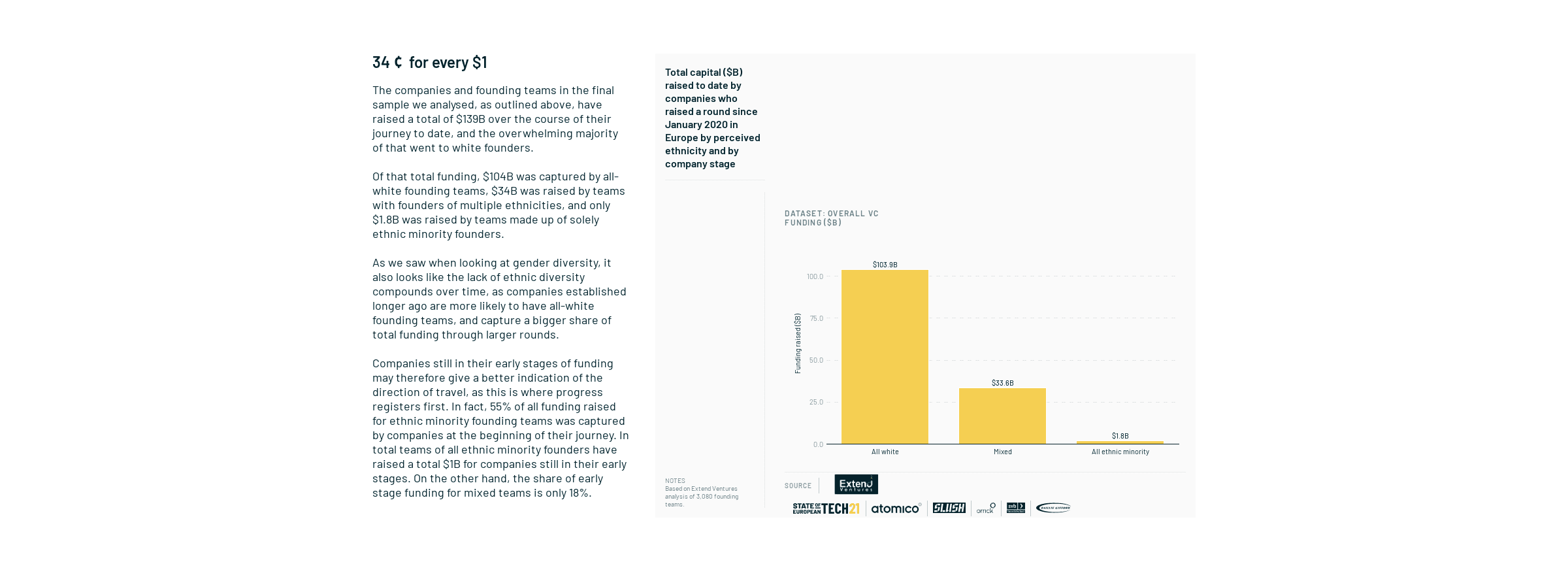

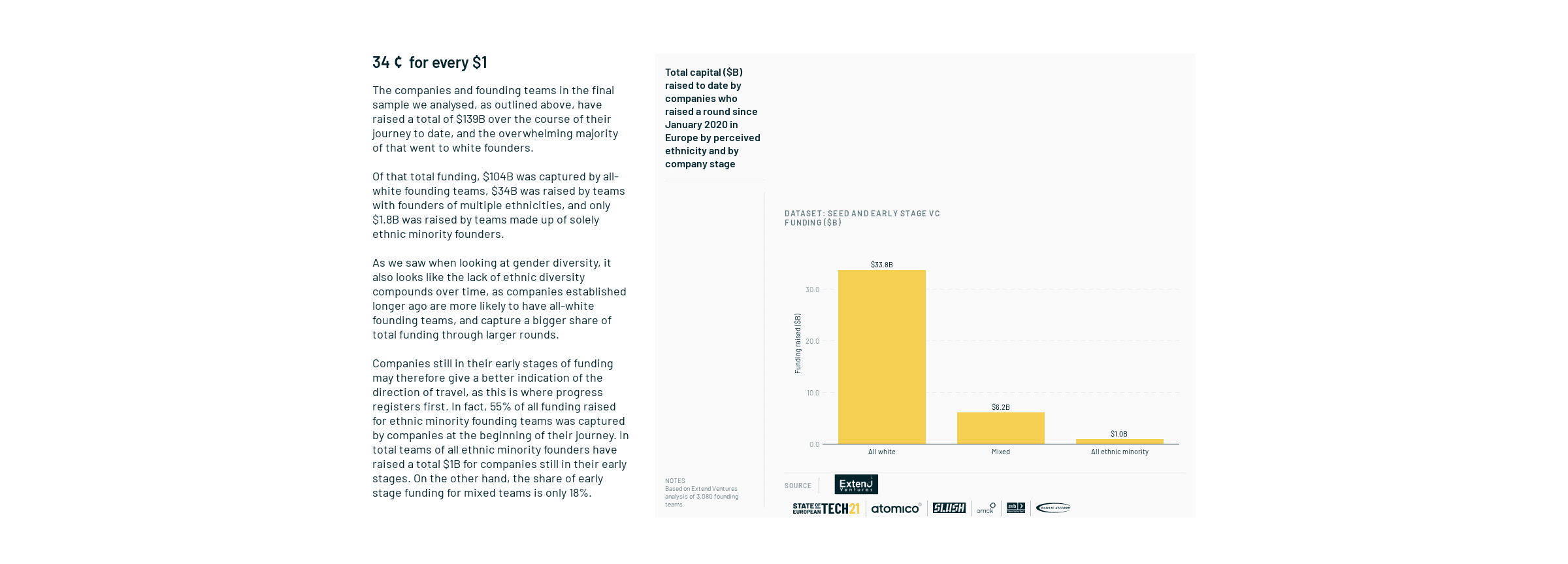

The story is similar when it comes to ethnic diversity. Founders from ethnic minority groups still face greater barriers to raising capital than white founders, with the majority of VC funding going to all-white founded companies. However, 55% of all funding raised for ethnic minority founding teams was captured by companies at the beginning of their journey. This indicates a more positive trend of increased investment for ethnic minority founded startups going forward.

In general though, Europe’s tech leaders, especially the young, are positive about Europe’s talent prospects. Europe has a highly-educated and highly-mobile talent pool. Founders are still finding it hard to acquire new talent but, as physical location is losing importance – a trend accelerated by the pandemic – accessing talent could become easier. According to 50% of the survey respondents, existence of a physical office and the ability to relocate employees is now less important.

Europe is attracting world-class investors

VC has become the leading funding mechanism for entrepreneurs, and as the opportunity set matures, Europe is seeing more international investors and buyers, from seed rounds to public markets. European VC is now beating US VC and European PE. This is causing more competition for investment – particularly at Seed stage, where 93% of respondents reported increased intensity in 2021, compared to 57% in 2020. This is leading to value inflation.

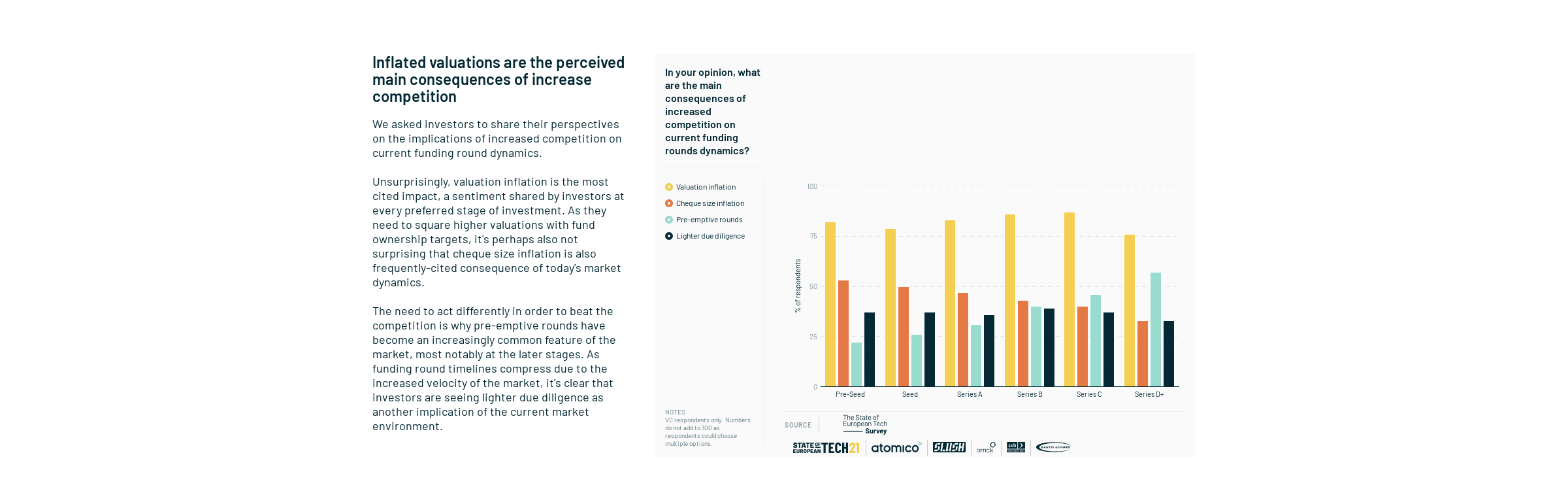

With increased competition, VCs are being forced to innovate. Over 90% of the VCs surveyed said that they were rolling out at least one new strategy, or change in strategy, to stay competitive. Pre-emptive rounds are one result of this, becoming an increasingly common feature of the market. Especially at the later stages. As the market speeds up and funding round timelines compress investors are seeing lighter due diligence as a consequence.

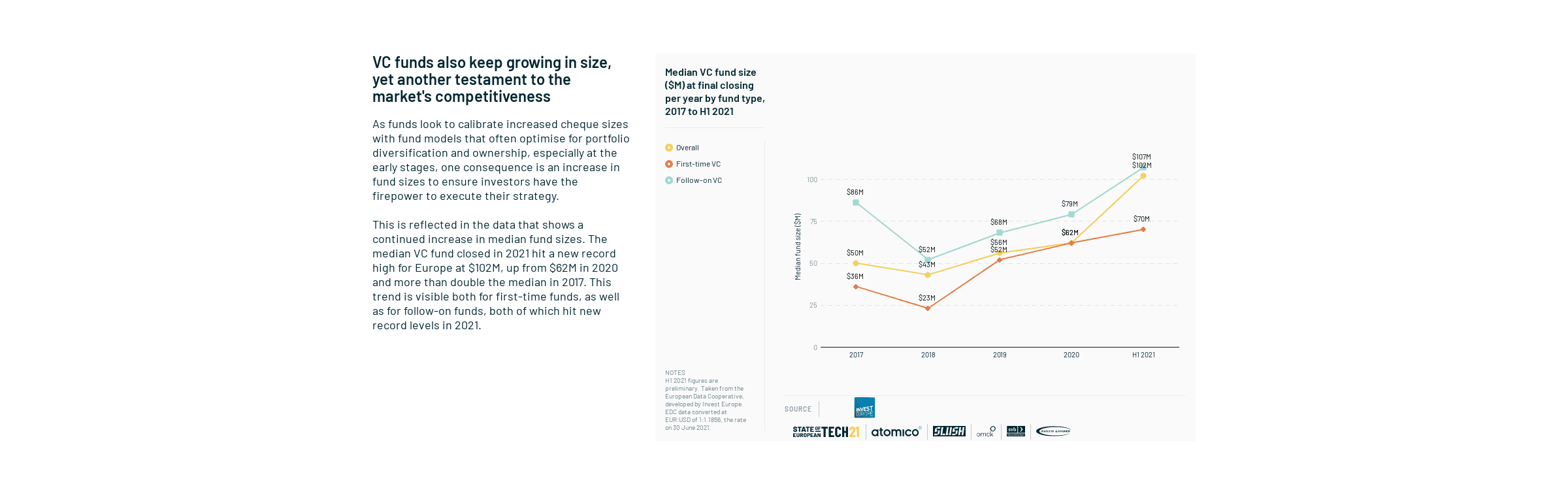

The market competitiveness is also seen in the fact that VC funds keep growing in size. The median VC fund closed in 2021 hit a new record high for Europe at $102m – up from $62M in 2020 and more than double the median in 2017. This trend is reflected in both first-time funds, as well as for follow-on funds, both of which hit record levels in 2021.

How does the future of European Tech look?

European tech is on a strong trajectory, with venture capital delivering consistently benchmark-beating returns. To continue the success in future, Atomica’s report found that more emphasis needs to be placed on fine tuning funding, talent and policy.

Regulation is perceived as one of the biggest challenges facing the European tech ecosystem – founders placed it second only to funding in terms of challenges. However, there are signs of progress within the regulatory environment. Whilst the majority (54%) of founder and leader respondents felt the regulatory landscape had stayed the same, 26% felt it had improved for the better.

When it comes to employment within the tech sector, growth has been incredible in 2021. Whilst European employment as a whole has grown by 0.4% over the past 24 months, startup employment has grown by 19.4%, adding around 400K new roles. And, year on year growth hit a record 10.9% in 2021. Despite this growth, diversity is still an issue and, according to the report, this is something that founders and investors need to prioritise to make sure the problem doesn’t get any bigger.

Overall Atomica’s annual report shows that European Tech is in the strongest position it has ever been, with positive signs for the future too. But, as with other markets and industries, there is still improvement to be made.