Every entrepreneur knows this feeling. You have launched a killer product and got some early traction. You are ready to put yourself out there and blow VCs away with your vision on how you will change the world. Instead, they are immediately bombarding you with KPI questions, mainly trying to understand if your product can become a good business as well…

by: Yannick Oswald

photo: Kaori Anne Jolliffe

featured: Yannick Oswald

The question most investors love to ask first is: ‘What’s your churn?’ And this even more so in times of COVID 19. Ah, and yes, ‘do you have a smile!?’

Let me kick off this post with a somewhat contrarian statement.

In the early stage consumer world, universal churn is a bulls*** metric.

Churn is one of the most misunderstood numbers in consumer investing. Think about it. Churn is the rate at which customers are leaving you as a percentage of your total customers. Investors calculate this percentage as a total across all user cohorts. But, your consumers are tens of thousands of different individuals at many different moments of their relationship of getting to know you. Using one universal number, of one period of time, for all these users, just misses what’s actually going on underneath the data. This is especially true in the early days of a company. To analyze the health of a consumer business, we need to look at subsets of cohorts (at first weekly, then monthly, aso.) and try to understand each cohort’s core engagement and retention.

Let’s take a step back. Why are investors so obsessed with churn, at first?

Because it is impossible to scale a business if you are churning too many users.

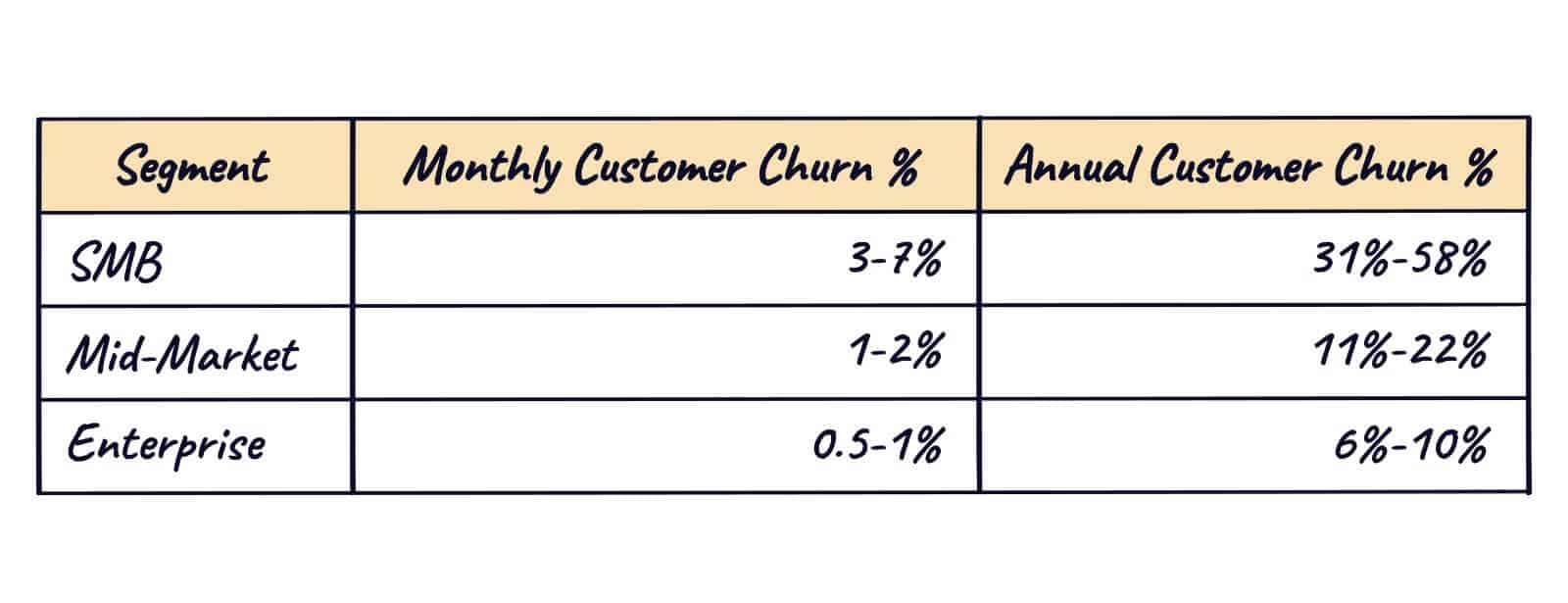

Once you are paying for user acquisition, as most startups do in search of growth, churn is the single most critical metric that determines the success of your business. This is especially true for consumer plays. Here some #B2B #SaaS customer churn benchmarks. As you can see, the smaller the target customers, the higher the churn.

B2C SaaS businesses typically are at the higher end. On top, contrary to B2C SaaS companies, B2B players can (more than) offset customer churn through revenue upselling, leading to negative net churn.

With the rise of D2C subscription services such as meal (think Blue Apron) or personal care products (think Dollar Shave Club) delivery services, investors became even more obsessed with churn. It became clear that many of them don’t have a sustainable business model. On top of the staggering acquisition costs, retention was just not high enough. And once these services lost their expensive customers, it isn’t easy to regain them.

Average net monthly churn rates of 5% or less are considered to be best in class for consumer subs. The biggest winners are usually even well below 5% at scale.

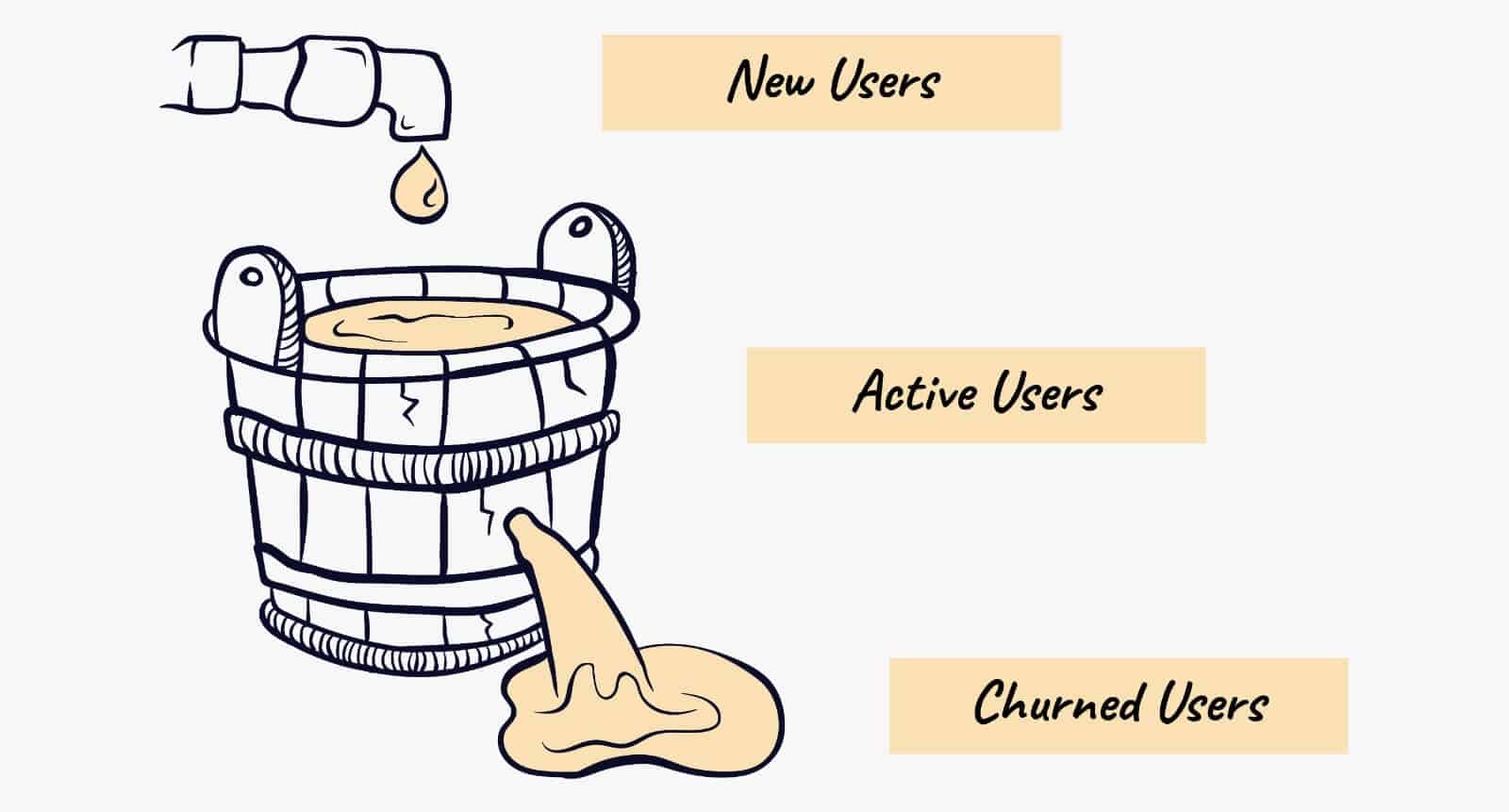

To understand investors, think about your service as a leaking bucket.

Each month, you spend money to acquire new customers. Those new subscribers are placed in the top of your bucket. Churn is the hole in the bottom of the bucket. If your churn is too high, it doesn’t matter how many new subs you put in the top…

Growth can have a nasty effect. The bigger you get, the more customers you lose (and have to replace) every month. A 10% monthly churn rate, when you only have 50,000 subs, means you only lose (and have to replace) 5000 subs a month. But 10% churn when you have 500,000 subs, means 50,000 new subs are needed per month, just to tread water…

A churn rate of 10% a month essentially means you lose (the equivalent of) ALL of your customers every 10 months. Those businesses are just not sustainable. You might have a product or service that some customers want, but you are selling it to them in the wrong model. Your customers are telling you they don’t want to buy every month.

The B2C SaaS reality

Besides retention being even more critical than in the B2B world, B2C SaaS requires some fundamental assumption changes.

(1) One common misconception is that churn is a reaction to your value proposition after people have discovered your product or service. If it is high, you have a problem. Well, not in the B2C SaaS world. Whatever the reasons, you will lose a big chunk of your users in the early days as they are getting to know you. Just take a look at the free trial to paid subs conversion of some of the biggest content platforms out there. Do not freak out, but up to half of this drop often happens on day 1.

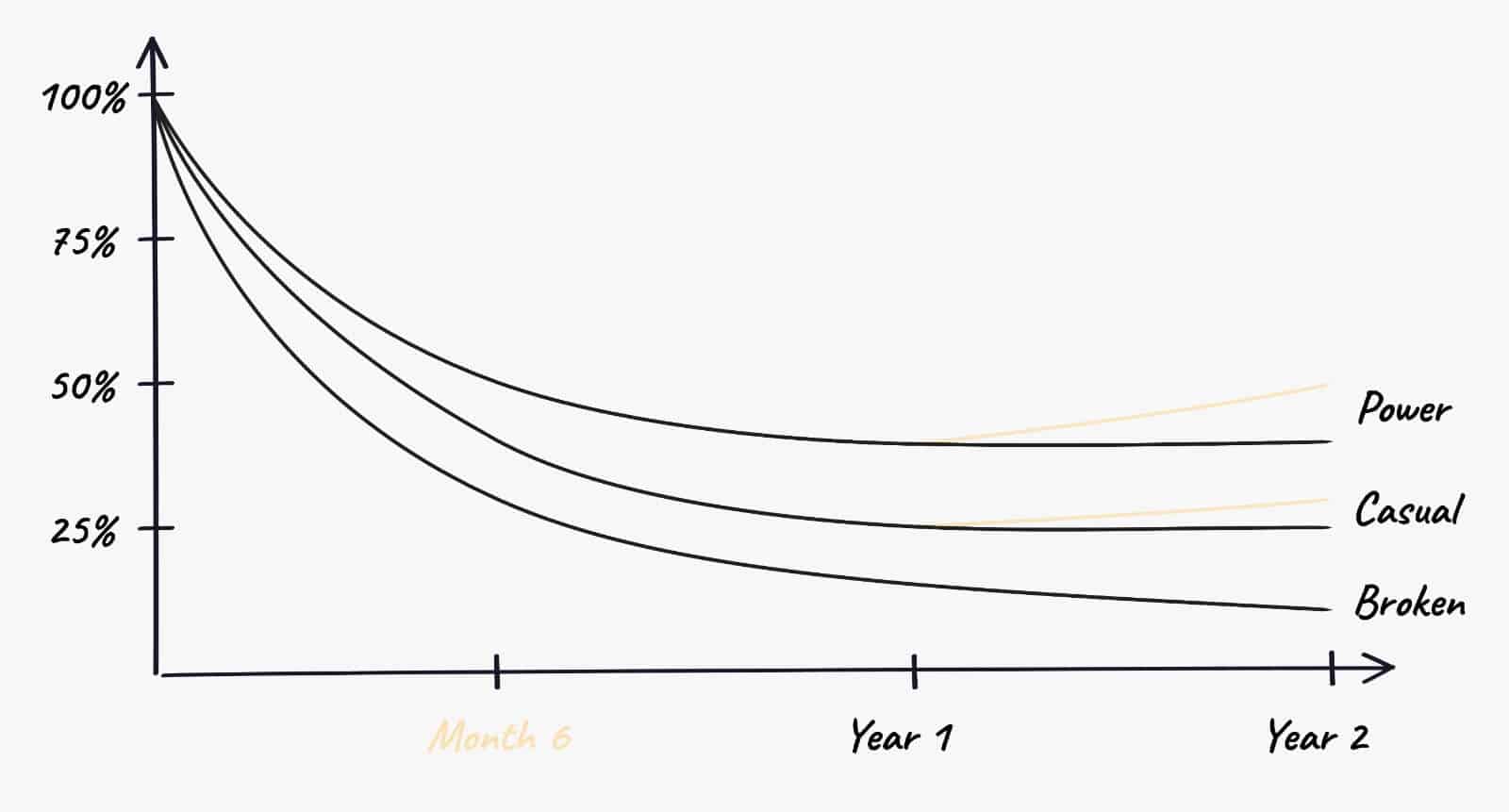

What is important to watch is what happens after the onboarding period. After they had a chance to really get to know you, the usage of some of your customers starts to become highly predictable and stable over time. This asymptote is what every consumer business is thriving for (see graph below). It means that users are endorsing your value prop. The exact level of this line flattening does not matter, as long as your CAC is in sync.

(2) A focus on monthly churn doesn’t make sense. Long term cohort retention is what matters. The best B2C SaaS businesses have a majority of annual subs. The rule of thumb is to aim for 80% annual subs. Therefore, while churn is typically linear for B2B SaaS companies, this is not the case for B2C SaaS. After the trial drop, another significant drop is to be expected after Year 1. The users that stick around after that are the ones that matter. Gross retention is then starting to look similar to B2B. On top, the Apple store commission drops from 30% to 15% after Year 1. Ultimately, this means that most of the LT ARR is driven post Year 1 by long term sticky user cohorts. To offset this Year 1 churn is also the reason why the best founders are trying to break-even on marketing on Day 1.

(3) But how can I raise money if it takes me more than a year to figure this out? Well, you need to predict churn before it happens. To do so, you need to analyze user cohorts meticulously. As I said earlier, it does not make sense to use one churn metric for all users. Instead, break your weekly and monthly cohorts up according to user engagement and make retention assumptions. Usually, you need at least 4-6 months of data to do so properly.

Power users: They are so engaged with the product that the likelihood for them to stick around in the long term is very high.

Casual users: They are engaged but use the product infrequently. How you build a better relationship with them? What % of them do so?

Broken users: They will likely churn. Run some winback campaigns. Notify them if they still have the app installed. Send a targeted email. Run a loyalty program. Winning back users can be a lot more cost-effective than acquiring new ones.

When too many of your users are likely to churn after Year 1, you have a problem. My colleague Roy calls this broken SaaS. Stop growing and focus on your product because high churn will eventually bite you in the a**…

(4) Make sure you are focused on the RIGHT core action to measure user engagement. And FOCUS on it.

The core action is the action most correlated with retention. Many entrepreneurs are focusing on the number of times users engage with their product vs. the number of times users complete a core action. The core action is the action that forms the foundation of your product. For example, in the case of our audio entertainment company Sybel, a core action is to complete listening to an entire episode vs. only opening the app or start listening to an episode.

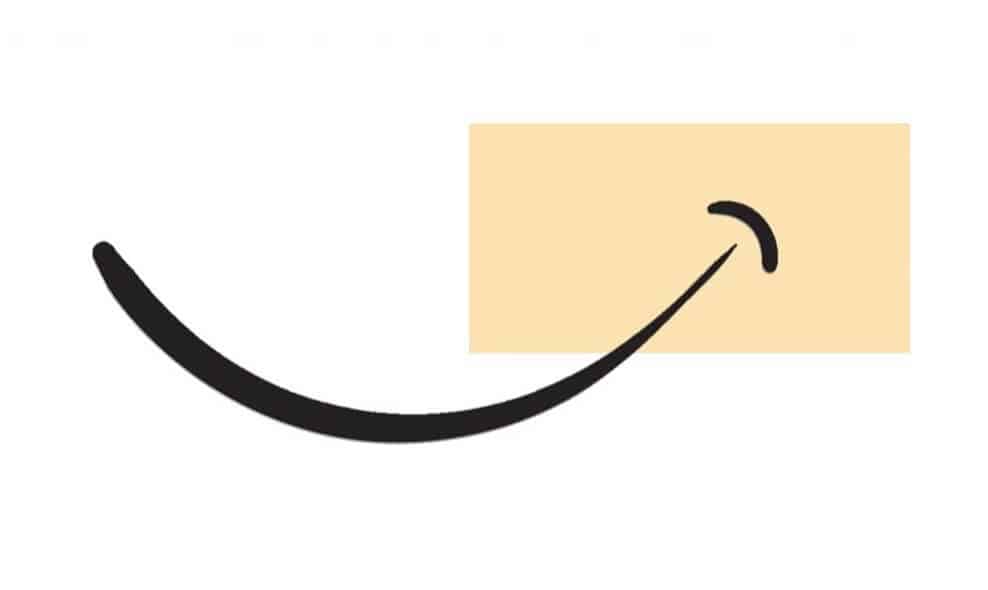

As your product evolves, cohort engagement and retention should increase over time, especially for the power users. Create accruing benefits and mounting losses as a user engages. Just think about how Spotify’s hook – recommendations and playlists get better and better over time. Have a look at the arrows to understand how investors will read your engagement and retention cohorts.

You may even see a bit of a smile for some user cohorts. As users are getting to know you better, engagement might even increase over time. In the very best case (but it is very rare), you can upsell new features and drive negative net revenue churn in the long term.

(5) Make sure you have your retention under control when raising a Series A.

Even if we have seen some of our companies do it, most businesses that show high churn in their early stages will not meaningfully reduce it. In general, you can expect your optimization efforts to maybe move churn by 1% to 2%, but usually, they won’t cut it dramatically beyond this. This is because churn is a statement from your customers about how habitually valuable your service is to them. The only way to meaningfully reduce churn in high-churn businesses is to fundamentally redesign the service. What is your experience? Please share your learnings in the comments below.

It all comes back to stepping on the gas before finding product-market fit… Make sure you identify and understand your power and casual users early on.

***

Recent content that I have found useful:

– We are proud investors in Anthony Watson’s company TBOL and super stoked for him to make this list of LGBTQ business & tech leaders.

– Check out this podcast with my partner Mark. He shares some great insights on how to fundraise during COVID 19, the importance of stock options, and how our experience with our decacorn WIX shaped our thinking. Enjoy!

– Here some interesting notes from Salesforce’s Q1 earnings call last week. Enterprises continue to buy software. Salesforce is seeing higher close rates and increasing sales pipelines including large enterprise contracts.

– My podcast (in French) with the team at BabyVc. We talked about our Pan European approach as an early-stage investor, areas that I am excited about, and some other cool topics. Check it out.

– Interesting take on the unbundling of Zoom. Many use cases like telemedicine, fitness, education have been force-fitted on top of Zoom. Looking out, each use case will have its own set of apps, custom-built from the ground up. Will the growth of the Zoom app itself be far outstripped by the growth of “the rest”? More on that in a later post.

– Free Cash Flow is king = One of the reasons why Zoom is killing it. Every startup, eventually needs to pay the piper this way. Key word here is eventually! And if growth investors don’t bless a startup, the answer is simply earlier.

– Microsoft invested in Facebook in 2007. How did that play out? And how did an unknown investor from Russia came out of nowhere two years later to lead the Series D.

– Have a look at this chart. Restaurant bookings in Germany are back to pre-Covid levels, while the US and UK are still at below -80%.

– Speed is everything. How many clicks do you need to create an account in Revolut vs. other banks? Revolut’s onboarding is killing it… Now it is time to build a great business as well.

– A great survey on LP Sentiment Survey on Alternative Assets by the Kauffman Fellow Journal. Overall, pretty positive survey results considering the circumstances.

– ‘The API-as-a-marketplace‘, a great read by Version One on how an “API-as-a-marketplace” works and what makes this opportunity so unique. This is an early but super-interesting trend.

– A new B2C SaaS acquisition: Mathway got acquired by Chegg for $100m in cash + $15m earn-out. At $13m net revenue in ‘19 and assuming a bold 2x growth rate in ‘20 that would a 4.4x net run rate revenue multiple.

– Are VCs still investing? A great analysis by Christoph based on Crunchbase data.

Check out Yannick’s blog. Reach out to him. Share your comments.