Many entrepreneurs from around Europe reached out to me over the last weeks, all with one question: “What is going on in VC right now?” Here are some clarifications.

While 2022 should have just been a transition year to normalcy, the economic crisis now hit even the last outposts of the tech world instead. All the big names see their stocks decline massively (except Apple whose stock is holding up), and the private markets funding crunch now entered the earlier stages as well. Only the ‘crème de la crème’ with massive market potential will still get valuations somewhat close to what we have seen in the last few years. It feels like the final wake-up call for those who didn’t get the memo yet. The keyword is ‘short-term volatility’. But make no mistake, mid- to long-term, tech will continue to dominate and drive the majority of economic growth around the globe.

What is happening in the market?

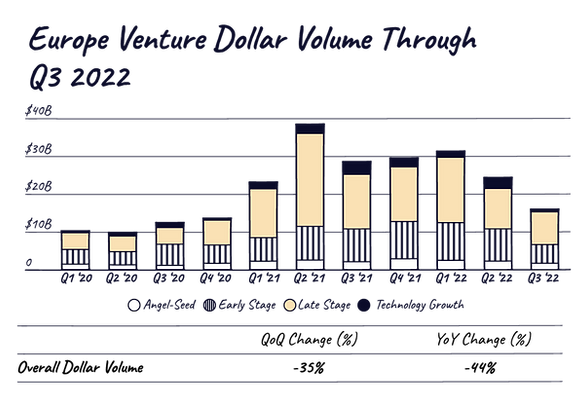

The ‘big party’ of the past few years is surely over in venture funding. After early-stage startups were raising significant amounts even pre-product, and big and small tech companies went on unprecedented hiring sprees, the funding environment has substantially cooled down. European venture funding continued to fall in Q3 2022, sliding to its lowest point in nearly two years. In the past quarter, funding in Europe totaled $16B, down 44% year over year and 35% quarter over quarter. This downward trend is in line with what we’re seeing in North America and other parts of the world.

While the decline at the later stages was apparent already earlier this year, the biggest dip quarter over quarter was at early-stage funding (down 40%) to below $5B. The ‘late stage’ still fell by a greater proportion year over year (and with it the number of new unicorns), but the ‘early stage’ will follow suit. This is normal, as the impact of the public markets takes time to tickle down. Therefore, it is not surprising that year over year seed-stage and angel funding fell by a lesser proportion compared to the rest and is ‘only’ down 29% quarter over quarter (largest drop so far though) and 20% year over year. Even though these are lagging indicators, it is now clear that European VC firms across stages have scaled back their investment pace. We are still above 2020 quarterly levels, so we should expect the downward trend to continue further.

What does this mean for tech founders?

We are all confused by the current environment: On the one hand, there are record levels of ‘dry powder’. On the other hand, there is less financing. Some founders might be wondering about the renewed emphasis on profitability after years of ‘growth at all costs’. At the same time, deal structures are starting to look different. So what does this all mean for tech founders? Here are some clarifications.

To be clear: Great companies will still get funded in the current market. Closing a round takes longer, and valuations are lower – but they are still happening. Median and average seed and Series A funding rounds have actually held up so far in 2022 compared to 2021 amounts. Median and average funding from Series B onwards declined. My feeling is that Q4 data will show a downward trend. If you are planning to raise a financing round, reach out to VCs early, build trust, and convince them that your business is the real deal. This will likely continue until the end of 2024 as public markets will not recover until the end of 2023/early 2024.

Weathering the storm

Even though times are tough, there is no fair or unfair. The frustration and exhaustion you might feel right now as a founder are common to everyone. This is not specific to your business. There is really no upside in complaining and dragging out the hard decisions. We all signed up for this when we joined the startup world. So let’s get over it, do what has to be done, and get back to building.

We all have to adapt our plans to weather the storm. Every business is different, of course (nice-to-have vs. must-have, cash in the bank or not so much left, high margin vs. low margin, etc.). At the end of the day, it is simple: What targets put you in the best possible position to raise your next round while not being overly reliant on external capital in the next 18 months? Every sales pipeline is getting re-evaluated, and every sales target is looking a bit too optimistic right now. No one is ‘killing it.’ This means that your situation is probably better than you think it is – on a relative basis.

But, even in a difficult market like the one we currently experience, it is a great time to hire brilliant talent, especially at the early stage. Nothing is lost, nothing is created. There is so much great talent out there today, and many want to get back into the office to join ambitious startups and company cultures. If you’re thinking of starting a company, then this might be the best period in a long time to launch a new company and build a great product. You don’t have to raise massive seed rounds anymore (at bloated valuations that put your cap table at risk in the mid-term) to be able to build your fundamentals.

There is no room for long-term pessimism

When we look at the broader picture of innovation capital, this is really just a blip. And, by definition, a blip is short – even though it might mean ‘a few years’. After all, we are already a year into this one. There is no room for long-term pessimism in technology. Downturns come and go, but innovation will always represent an outsized proportion of economic growth. Most importantly, tech and internet companies continue their unstoppable growth. In the last four years, the internet economy grew seven times faster than the total U.S. economy, now accounting for 12% of GDP. Yes, 2023 will be hard. But there are many reasons to be optimistic. Our Mangrove portfolio companies continue to raise capital and can hire better talent. Not only is tech penetration accelerating, but it is very early days.

Here is some perspective: Cloud computing penetration is only at 10-15% in the most developed economies, and overall digitization across sectors is at around 30-35% only. Think about healthcare, education, space, big data, encryption, online content distribution and compensation, banking, etc. There is a lot of room for innovation. I would argue that we are very lucky to be alive right now. In the grand scheme of things, global quality of life has dramatically improved in the past decades. Innovative technologies played a crucial role in solving challenges like extreme poverty. That is not to say that everything is perfect right now: Social mobility is stagnating, and equality of opportunity has receded in many developed countries. But if I have to take a bet, it will always be on tech. I am personally more pumped than ever to play in this market.

→ Want to know more about the recent market dynamics and why only continued innovation can be the answer? Head over to Yannick Oswald‘s blog ‘Opportunities Everywhere’ to read his newest article in full length.